You can tell a CEO who’s spent too much time ‘in the cloud’. They believe their own customer satisfaction surveys. Either that or they are deliberately gas-lighting us. To improve customer experience, Mobile Europe sought simple ‘people pleasing’ advice for telcos from people who really know the customer. In the first of an occasional series, Maria Harju, Foundever’s Chief Revenue Officer for Europe, the Middle East and Africa, describes The Seven Deadliest Customer Experiences and how mobile network operators can avoid them.

Repetition.

Repeating your story to multiple people is enough to make 57% of Europeans hang up. Yes, some problems demand escalation, but if you’re moving your customer across an omnichannel platform it’s omni stupid not to move the information from channel to channel too. A CX should systematically do that. This averts another massive frustration, disregard for the customer’s history. How can you pretend to care about the customer experience when you show you are demonstrably oblivious to it? All the information across all channels is captured and should be correctly stored and retrieved so that your agents can do their best jobs.

Rate your experience.

OK, we need performance feedback, but customers are suffering from survey overload. Every trip to the toilet now involves an invitation to rate the experience. There are better ways to learn how customers feel about service and how they perceive your brand. Speech and text analytics are instant, less obtrusive and more accurate.

Chatnots.

If you don’t acknowledge your chatbot’s limitations, you’re setting your brand up for a CX failure. If your customer knows it’s an automated system, they’ll treat it as such and adjust their expectations accordingly. But when the bot goes beyond its domain intelligence it must hand off to a live representative and pass on the information shared up to that point.

Chats …. with delayed response. Chat’s rationale is about immediacy and accuracy but long wait times and vague unfocused responses will demolish that advantage. Immediate contextual support can help a customer take action or make a decision. Avoid the temptation to set high chat concurrency targets for agents. The more conversations they handle the less likely they are to resolve complex issues or satisfy each customer. Use your best pre-scripted responses in early conversational stages so that agents have more time to find a resolution. Cross train your CX staff so that they can work across channels based on peaks in demand.

Undervaluing CX

If each interaction doesn’t meet expectations it will damage your brand. So stress its value in your proposition. A superior customer experience should be reflected in the price of a product or service. If you’re cheap very hard to hold on to customers, especially in the current economic environment. Here is the value of CX. Three in four consumers will walk after a single disappointing customer experience, yet 42% would pay more for an identical product or service if it were supported by a superior CX. Being in the latter camp starts with understanding who your customers are, their wants, needs and expectations.

Treating vocal interaction like a necessary evil.

Test yourself before you test their patience. Voice is about people not managing processes, so IVR should solve customers’ problems, not stress test their patience and short-term memory on the altar of your management processes, said Harju. Most consumers are frustrated by complicated menus then agitated by the agent that takes over. A happy resolution is an uphill battle. An IVR should minimise menu options, as part of the identification or authentication process so that more of the conversation is focused on the customer and their issue, and use it to coach the customer. Rather than playing a message saying the call is important, a message asking if a person has the reference number or other relevant information to hand is going to make everyone’s life easier.

Kyivstar’s CEO and CTO talk about the power of grit and operators pulling together

In a small, quiet meeting room on the sidelines of Mobile World Congress with executives from Ukraine’s largest operator Kyivstar, the discussion was in stark contrast to what was going on at the show. While other European operators talked about fair-share politics and future immersive experiences, Kyivstar provided an update on how it has kept people safe and its network up and running after one year of war.

Oleksandr Komarov, Chief Executive of Kyivstar, acknowledged having a somewhat “alien” feeling here as the operator has “very different challenges and priorities” compared to the rest of the industry.

In an interview with Mobile Europe, Komarov and Volodymyr Lutchenko, Chief Technology Officer at Kyivstar, shared how network resilience challenges have changed dramatically over the last year and how people have pulled together to preserve communications services. (Also see Telecoms in time of war)

National roaming

Cooperation among the country’s three operators – Kyivstar, Vodafone Ukraine, and Lifecell – has been “essential” for overall network resilience, and they have been “exchanging capacity and providing equipment to one another,” said Komarov.

Indeed, one of the first and most important steps the operators took after Russia invaded a year ago was to implement national roaming, so that if network services are down on one network, users are automatically switched to another. National roaming is unusual and difficult, but the Ukrainian operators were able to launch it in about three weeks with support from the national regulator.

The service is “working well to keep services going,” said Lutchenko. When the country suffered power blackouts in November last year, he said more than 2 million people per day used the national roaming service.

When the war started, the government also issued additional frequencies free of charge to the operators to give them extra network capacity. Meanwhile, equipment suppliers and local businesses have also rallied to help keep the networks going.

Komarov cited an example where Ericsson stepped up to support a “very big ambitious project to roll out a national core site in the western part of Ukraine … to mitigate the risks related to the potential loss” of other sites, he said. In peace time, such a project would take 12 to 18 months. But with everyone cooperating, he said they started the project at the start of 2022 and it was completed in early May, taking less than five months for a major deployment.

Moving targets for resilience

As the months of war have dragged on, the network resilience challenges have changed. In the first few months, Lutchenko said Kyivstar was engaged in “urgent activities” to keep the network going when the infrastructure was physically damaged by rockets, bombs, mines, and tanks, because the biggest problem is that it is often too dangerous to get to the sites to repair damages.

“[The sites] could be in occupied territory or on the front line. The area could be under fire or the fields can be mined so that without supervision from the military, you cannot get there … That’s why your network should be very reliable and still work with multiple damages like ours,” said Lutchenko.

Later in the summer, the resiliency work shifted to “stabilisation” projects. By September, Kyivstar’s network performance KPIs remarkably were “almost on a pre-war level.” Apart from occupied areas where Kyivstar had no access to sites, “the network was really good,” he said.

Attacks on energy pose new threats

The communications resiliency landscape changed in October when Russia started attacking the country’s energy infrastructure. Lutchenko said the challenge is now “really huge” and the “new reality.” In late October, about 20% of Kyivstar’s base stations were affected by power outages. Lutchenko said the worst day was November 24, 2022, when 65% of Kyivstar’s network was without electricity.

In response, Kyivstar has strengthened energy resilience by adding longer-life backup batteries and diesel-powered generators.

Here again, cooperation has been vital. In Kyivstar has “crowd-sourced” access to power generators from local businesses, such as a petrol station located near one of the operator’s cell sites. “We asked businesses and invited people to help us with keeping the network up and running,” said Lutchenko, and now more than 600 sites are connected to diesel generators.

But this is one area where Komarov feels help from the government has been “limited”. Of Kyivstar’s 1500 generators, he said about 40 were provided by the government and the rest were either procured by the operator or acquired from third parties that have “extra power capacity on hand located nearby our sites.” Kyivstar said it has invested around US$5 million just on generators and diesel fuel.

Fighting on two fronts

Kyivstar’s network is under threat from cyberattacks as well as physical attacks. “The Russians want to destroy us not only physically, but virtually as well, so that means we have to fight on two front lines,” said Lutchenko.

The operator took measures to protect its network by relocating certain equipment away from areas that were likely to come under Russian control. Komarov explained that in occupied territories there was a cyber defense effort underway to ensure that despite not having control of all its network, the operator was not “vulnerable to extra threats.”

“We streamlined the architecture of our core infrastructure to minimise the number of potential vulnerabilities,” he said. In Kherson, for example, Kyivstar had “just a media gateway and RAN network” and this “decreased the risk of penetration,” he said.

Restoring liberated areas

As territories are liberated, Kyivstar works on repairing the destruction to its network. Lutchenko said that about 18% to 20% of the telecom infrastructure in formerly occupied regions is “totally destroyed,” meaning “there is nothing from an equipment or infrastructure point of view.” About 30% to 35% is “heavily damaged” and about 40% has “minor damages.” Kyivstar says it can repair nearly 90% of the network in those areas.

“We’re waiting for our military to liberate more territory and we are ready to restore everything,” said Lutchenko.

Losing more than infrastructure

Kyvistar is worried about losing more county’s critical communications infrastructure: it is also working to keep its 3,800 employees and their families safe. In the initial months of the war, the operator provided instructions for where people could go for safety and converted regional offices into temporary homes with showers and washing machines for displaced families.

Around 140 Kyivstar employees have been drafted into the army and thousands volunteer to help the army in various roles. The operator has lost three of its employees in the war and two are missing.

Kyivstar relies on maintenance and construction suppliers, but their situation is “very much worse” because they cannot protect employees “with the same efficiency as Kyivstar” due to its critical infrastructure status, explained Komarov.

Lutchenko joined Kyivstar in November 2021 and has been in the telecom industry in Ukraine for more than 25 years. “I don’t think anyone can plan for stuff like this. The most important thing is we have the greatest team in the world.”

Asked how the war has affected the operator’s business, Komarov said the operator was “in the green” and there is “extremely high pressure on our networks.”

“But let’s face it, it’s less about business and much more about survival,” he said.

Microsoft, VMware, Intel, AMD and OneWeb are the latest to stop trading with Russia – and some with Belarus too

Last week Google blocked Russians’ access to Google Pay and Apple did likewise with its wallet product and product sales in Russia.

Some have criticised Apple’s move, pointing out it could push people towards using Android phones made in China that are more susceptible to hacking and surveillance.

However, Apple made the moves after a direct appeal to its CEO, Tim Cook, by the Vice Prime Minister of Ukraine Vice

Now more big tech firms are following their lead.

Microsoft has suspended all new sales of Microsoft products and services in Russia.

The chips are down

Chip giant Intel said in a statement that it, “condemns the invasion of Ukraine by Russia and we have suspended all shipments to customers in both Russia and Belarus.

“Our thoughts are with everyone who has been impacted by this war, including the people of Ukraine and the surrounding countries and all those around the world with family, friends and loved ones in the region.”

Another chip giant, AMD has also stopped shipments to Russia and Belarus.

VMWare is suspending all its business activities in Russia and Belarus due to the unprovoked attack by Russia. It published a statement that read, “We stand with Ukraine, and we commend the bravery of the Ukrainian people. The human toll is devastating and like other global businesses, we are committed to supporting our Ukrainian team members, customers and partners.”

It added, “We are also seeking to support non-Ukraine-based employees with family members located in Ukraine with information to access available resources. We continue to support our employees in Russia, as they are adversely impacted by the consequences of their government’s actions.

“The suspension of operations includes suspension of all sales, support, and professional services in both countries in line with VMware’s commitment to comply with sanctions and restrictions.”

The board of directors at satellite operator OneWeb has voted to suspend all launches from Baikonur, the Russian cosmodrome in Kazakhstan.

Social media battles

Meanwhile social media sites are continuing their battle with Russian authorities, which are keen to control the flow of information and the narrative surrounding the war.

Facebook, Twitter and YouTube have acted to prevent Russia’s state media making money from ads on their sites. In response, Moscow has said will restrict access to Facebook after its parent company Meta refused to stop fact-checking some Russian media companies’ output.

TikTok has limited access to Russian state-controlled media accounts in the EU and Reddit has stopped users posting links to Russian state-sponsored media.

NRB acquired 20MHz in the 3600MHz band to offer 5G directly to its customers but has now decided to embrace the MVNO model

Belgium’s former incumbent, Proximus, it looking to acquire more 5G spectrum from NRB in the 3600MHz range. Proximus says the acquisition will support its “ambition to continue to offer the best mobile experience in Belgium for decades to come”.

NRB is selling its 5G licence to refocus on its core business, while maintaining its commitment to offering 5G services. The companies are discussing a possible wholesale agreement.

The NRB Group is one of the biggest ICT firms in the country and serves public and private sectors organisations in Europe. In 2022, it had revenues of €505.4 million and more than 3,450 employees.

Spectrum auction in 2022

When the 5G spectrum was auctioned in the summer of 2022, Proximus decided to invest €600 million over 20 years.

At the same auction, NRB acquired 20 MHz in the 3600MHz frequency band to provide 5G services to customers in the public and social sector, industry and biotech, energy and public utilities, financial organisations and insurance companies.

Now the Belgian company has decided against rolling out its own mobile network, but intends to continue offering 5G services to customers as an MVNO – possibly through a partnership with Proximus.

Raising the limit

Acquiring the additional 20 MHz in the 3600 MHz band would give Proximus a total of 120 MHz so that the operator could add more capacity where needed. In future, it could be used to improve throughput and latency, as well as the security of data flows on private mobile networks.

The agreement between Proximus and NRB was submitted to the BIPT, the federal telecoms regulator. The latter has approved the transaction, subject to the effective transfer of rights taking place after the publication of a new call for applications for the 3410-3430 MHz band in the Belgian Official Journal.

That publication is imminent and the call for applications will be accompanied by an increase in the spectrum cap from 100MHz to 120 MHz to enable Proximus to acquire NRB’s 20 MHz.

SaaS provider Totogi claims total cost of ownership could fall by up to 80% as disaster recovery expenses are all but eliminated

Totogi’s Charging-as-a-Service platform has gone live for Zain Sudan which has more than more than 20 million subscribers. The country has a population of just over 49 million. According to the SaaS provider, the transition from the legacy charging system to the new platform took 18 days for Zain’s production and disaster recovery environments.

The expected benefits are up to 80% lower total cost of ownership (TCO). Totogi says the new platform has “nearly eliminated Zain’s disaster recovery expenses, slashing them to just a fraction of the previous cost of maintaining a backup service”.

Sudan has been ravaged by civil war between the country’s army and the paramilitary Rapid Support Forces (RSF) since April 2023 and it appears to be intensifying.

Totogi bills Zain on a pay-as-you-grow’ business basis and says this also allows the operator to scale as required while avoiding large upfront costs.

Totogi also claims that the cloud-native solution has “future-proofed” Zain’s BSS stack and offers better performance, reliance and compliance

Emad Elsheikh, CTO at Zain Sudan, commented, “Transitioning over 20 million subscribers to Totogi’s platform was executed with remarkable speed and efficiency, showcasing the agility and effectiveness of their solution in managing large-scale subscriber bases under demanding conditions, particularly in times of crisis when traditional on-prem systems are likely to fail”.

Zain Sudan is part of the Zain Group, which offers mobile voice and data services and started in Kuwait in 1983. It has opcos in seven Middle Eastern and African countries, providing services to more than 50.6 million individual and business customers as of the end of last year.

Despite a 19% drop in sales, Pekka Lundmark remains confident of a stronger second half and achieving the company’s full year outlook

Nokia CEO and president Pekka Lundmark reflected on what the company called a “challenging environment” after weaker sales in North America and India led to the vendor posting revenues of €4.67bn, down by almost one-fifth from a year ago.

However, big cost cuts – including October’s announcement it would cut up to 14,000 jobs out of 86,000 employees – meant the vendor ending up with a 52% rise in Q1 net profit (€438m). Gross margin improved significantly year-on-year, to 48.6%, due to a combination of an improved gross margin in Mobile Networks, and the three smartphone licensing deals signed in Nokia Technologies. The vendor ended the quarter with a net cash balance of €5.1 billion.

Like Ericsson earlier in the week, Lundmark has seen some second-half green-shoots stating: “continued improvement in order intake, meaning we remain confident in a stronger second half and achieving our full year outlook.”

Breaking this down, Nokia saw improved order intake trends in its Network Infrastructure business in Q1 – the book-to-bill ratios was above one. Lundmark said the outlook for Fixed Networks has improved over the past three months, adding it was usually the first market to recover. However Optical Networks was still looking weaker. As a result, he sees Network Infrastructure returning to growth in the full year.

In Mobile Networks, the end of the 5G growth spurt in India combined with ongoing low levels of activity in North America led to a 37% net sales decline in the quarter. Nokia said that while all regions remained weak it continued to see growth in Middle East and Africa.

Fixed line’s relative health

Lundmark said Nokia has more than 40% market share globally excluding China in OLT products. “With our product portfolio and the ability to offer customers a roadmap to deploy X GPON, XGS-PON, and 25G PON in the same line card, we have a compelling value proposition,” he said. “Customers can also upgrade to 50G and 100G in the same chassis down the line with our Lightspan MF-14 platform.”

He added: “It’s important to remember that globally excluding China over 70% of homes are still not connected by fibre and there is a significant opportunity remaining in our biggest markets of both North America and Europe… In Europe, we see deployments remaining at a high level in markets with low penetration and we are seeing some mature markets starting to upgrade to XGS-PON and 25G PON.”

Automation and reducing telco opex

The chief executive said Nokia now has the capability to drive zero-touch autonomous operations across all network domains, including managing autonomous operations across multi-vendor networks.

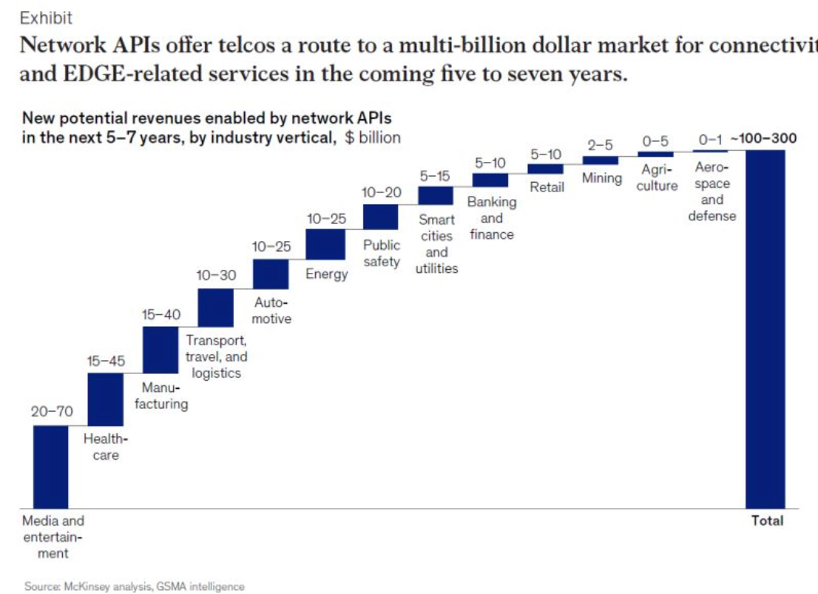

“We have customers who are purchasing our autonomous operations specifically to accelerate their API exposure strategy,” he said “Our holistic solution is what also enables network programmability and the ability for CSPs to expose their APIs to developers using our network as code platform. This is a key point and we already have 11 operator agreements for our platform.”

He added: “To fully benefit from the emerging network APIs, CSPs need their operations to be fully automated because the API paradigm assumes an application interacts directly with the network in real time.”

Dell partnership is strategic

Lundmark highlighted Nokia’s strategic partnership with Dell, announced at MWC, as something that will benefit the vendor’s mobile, cloud and network offerings. “On the Nokia side, we will now adopt Dell as our preferred infrastructure partner for existing Nokia AirFrame customers, which will enable us to refocus our R&D efforts into areas where we can really differentiate as Nokia,” he said.

“Secondly, our private wireless solution, NDAC, or Nokia Digital Automation Cloud, will become Dell’s preferred private wireless platform for enterprise customers,” he said. “And we can see this becoming a very powerful channel to further drive growth in private wireless.”

Displacing Huawei and replacing chips in China

The CEO told analysts that the move by operators to strip out Huawei equipment was a gradual process. “But in typical Chinese vendors account 20% to 30% in markets outside of China, outside of the US of course, we estimate that last year in Mobile Networks and network infrastructure, the Chinese vendors have roughly or had roughly €12 billion in sales outside of China,” he said.

“And about half which is €6 billion of that in Europe, and this is obviously an ongoing discussion in several European countries that how they should deal with that question. But gradually the importance of this opportunity for us is continuing to grow,” he added.

When asked about the recent Chinese Government stripping out foreign chips from the nation’s telecom equipment, Lundmark said Nokia had not seen any impact. “We still need more clarity around that statement, because there are so-called foreign chips in pretty much all parts of all networks,” he said. “So, it’s very hard to see what that would mean in practice. So, we need more clarity about that. But important for us is to of course remember that our market share in China is fairly low and China accounts only – Mainland, China accounts for a low single-digit percentage of our sales.”

Sunrise filed a complaint against Swisscom suggesting the telco had behaved improperly in the 2008 tender process to set up a broadband network at Swiss Post sites

Switzerland’s Federal Supreme Court has concluded that Swisscom’s conduct in the 2008 tendering process for the broadband networking of Swiss Post sites was fair. As a result of the decision in the long-running legal proceedings, last month the court upheld Swisscom’s appeal and overturned the original penalty decision of the Competition Commission (COMCO) from 2015, with the imposed fine of more than CHF 7 million, as well as a Federal Administrative Court judgement from 2021.

Swisscom welcomed the Federal Supreme Court’s ruling which also overturned the contested ruling of the Federal Administrative Court, which in 2021 concluded that the telco “behaved improperly” in the 2008 tender process to set up a broadband network at Swiss Post sites.

The Federal Supreme Court found that Swisscom did not force unreasonable prices on Sunrise or Swiss Post and demonstrated fair conduct in the setting of prices for wholesale products. Moreover, the prices charged by Swisscom for these wholesale products were not inflated.

In respect of Swiss Post, the Federal Supreme Court found that the bid price was the result of negotiations and was not set unilaterally by Swisscom. Finally, the court concluded that Swisscom had not imposed a margin squeeze on Sunrise and did not demonstrate anti-competitive conduct.

Long-running dispute

The proceedings date back to 2008 when Swiss Post had put out a call for tender to set up a broadband WAN between its sites. After a suitability test, it requested bids from Sunrise, UPC and Swisscom. It then accepted Swisscom’s bid in January 2009. Sunrise responded by filing a complaint against Swisscom with the competition authority, claiming that Swisscom had violated the Federal Cartel Act.

In September 2015, COMCO concluded that Swisscom had abused its market position, forced unreasonable prices from competitors and Swiss Post, and imposed a margin squeeze. In response, COMCO imposed a fine of CHF 7.9 million on Swisscom.

Swisscom contested COMCO’s decision

Swisscom said it had previously demonstrated to COMCO that Sunrise would have been able to submit a competitive bid if it had made “prudent use of its own and intermediate inputs”. The telco said in a statement: “The allegation of misconduct to the detriment of Swiss Post is also incomprehensible: as a powerful buyer, it had awarded the contract to the party submitting the most competitive bid, from its perspective, within the context of a GATT/WTO tendering process and in accordance with the strict rules that such a process entails.”

Swisscom subsequently lodged an appeal against the COMCO decision with the Federal Administrative Court. In June 2021, the Federal Administrative Court largely upheld the COMCO decision, but reduced the fine imposed to CHF 7.4 million. The Federal Administrative Court also concluded that Swisscom had behaved unlawfully in the tender for the broadband networking of postal sites to the detriment of Sunrise and Swiss Post.

Swisscom lodged an appeal with the Swiss Federal Supreme Court stating that it acted in accordance with the law during the tender process launched by Swiss Post, which requested bids from Swisscom and Sunrise.

Salty ending

In February, Swiss Post signed a strategic partnership with Salt to offer prepaid and postpaid “Post Mobile” services from its branches. Despite offering subscriptions, smartphones and telecom accessories from various providers in its branches for more than 20 years, Swiss Post has moved to a single partner. However, Swiss Post is still tied to Swisscom for several ICT services.

UK operator to use Starlink to reach underserved rural areas; IoT provider to offer fully managed combo of cellular and satellite connectivity to expand reach

Virgin Media O2 is using Starlink’s Low Earth Orbit (LEO) satellite technology to provide mobile backhaul for some of the country’s most remote locations to accelerate its Shared Rural Network (SRN) rollout.

The operator has deployed the Starlink for backhaul in the Scottish Highlands (pictured) which are difficult or impossible to connect using technologies like fibre or microwave connections.

Implementing satellite connections to these locations is after intensive testing and a successful recent trial in northern Scotland.

SRN behind schedule

This is the latest development in Virgin Media O2’s push to improve mobile signal in rural communities through the Shared Rural Network programme. With the exception of EE, the participants in the SRN are behind targets, according to the National Audit Office. Last October, Vodafone, Three and Virgin Media O2 reportedly asked the government for up to two more years to complete the first stage of the Shared Rural Network (SRN)

Virgin Media O2 is also exploring satellite connectivity for emergency services and to boost mobile connectivity at large events.

This Starlink project was delivered in collaboration with Telefónica Global Services (TGS). TGS is a subsidiary of Telefonica Group, which owns 50% of Virgin Media O2, and is an accredited Starlink reseller.

Jeanie York, Chief Technology Officer at Virgin Media O2, said, “By constantly finding new ways to deliver for our customers, we are bringing reliable mobile coverage to rural communities faster and helping to close the UK’s digital divide.”

Starlink and global IoT

Wireless Logic, a global IoT connectivity platform provider, has secured authorised reseller status for SpaceX’s Starlink LEO satellites. The agreement meansWireless Logic will integrated satellite connectivity into it portfolio of managed services. The rationale is to offer customers greater flexibility and choice for their global IoT deployments.

Wireless Logic’s specialist subsidiary Blue Wireless will deliver integrated, managed services combining LEO technology, LTE and 5G. It will offer data plans, installation and on-site support in more than 70 countries worldwide, with guaranteed service level agreements regarding uptime and speed.

Wireless Logic acquired Blue Wireless last year to strengthen its presence across the Asia-Pacific region and the Americas, as well as improving its fixed wireless access portfolio.

Unique proposition for industries

Oliver Tucker, CEO at Wireless Logic. “This milestone agreement underlines our commitment to innovation. While cellular remains a cornerstone for many applications, the addition of satellite connectivity is a game-changer – especially in challenging cross-border environments and areas of weak coverage.

Ivan Landen, CEO at Blue Wireless, said of the Starlink arrangement, “By harnessing the combined strength of 5G/LTE and satellite technologies, we can deliver a unique proposition for industries like energy, agriculture, mining, construction and maritime. This extends to other organisations needing resilient branch, portable or mobile connectivity.

“Our Global Managed LEO proposition helps global customers overcome typical challenges like procurement, installation, support and in-life performance.”

The operator panellists shared their candid experiences around how their service delivery and cultures are changing to stay competitive, internally and through partnerships

The discussion took place at our recent Telecom Europe Telco to Techco virtual event, moderated by CCS Insight consumer and connectivity director Kester Mann. Our panellists were Telefónica Germany VP director of massmarket Dr Mariam Kaynia, Vodafone Business head of digital Michelle Hastings and Intellias senior director telecom & media Ahmed Soliman.

Intellias’s Soliman said the adoption of current tools and open-source technology is vital for telcos to innovate and stay competitive. Despite the industry’s regulation constraints, integrating open-source solutions like OpenAI offers opportunities for advancement. Soliman also addressed the disparity in talent acquisition and flexibility between telcos and technology firms like hyperscalers. While the latter can readily acquire talent and pivot with ease, telcos face challenges in upskilling their workforce and adapting to rapid changes.

He underscored the importance of investment strategies, noting how technology companies have historically been quicker to identify and acquire innovative platforms like Skype and WhatsApp, revolutionising communication.

Hyperscaler competition has changed

Telefónica’s Kaynia agreed that telcos are slower than hyperscalers at this, but she said: “it’s simply because of our legacy landscape that makes it hard to adapt as fast as some of the others do.”

She also addressed the evolving relationship between telcos and hyperscalers in tackling enterprise networking requirements. Emphasising a spirit of partnership over competition, she highlighted the necessity of collaboration to meet the demands of a rapidly changing market.

“It’s not about comparing [to hyperscalers]. It’s a partnership that is required and this is how we also operate in the industry,” she said. “We are not competing, we are not trying to say take each other’s lunches, we actually need each other in order to be able to become more digital and more efficient and more agile towards our customers as a whole.”

Kaynia acknowledged the unique capabilities that hyperscalers bring to the table, emphasizing a desire to leverage these without duplicating efforts internally. Conversely, telcos offer expertise and established customer relationships that are invaluable in delivering comprehensive solutions.

“It’s really more about a hybrid collaboration across the whole system to bring together the different players need from cloud providers…solution providers…telcos…system integrators and only jointly can we really deliver what the market needs,” she said.

Addressing the complexities of the current landscape, she attributed much of the challenge to the rapid evolution of customer demands alongside the need for telcos to manage both stagnant revenues and increasing costs. “If you put the whole landscape together, it is more complex because you want to deliver more you want to do much more for our customers and be more agile and efficient and, at the same time, we need to manage the both revenue as well as the cost side of it,” she said.

Vodafone’s Hastings agreed that it is becoming increasingly clear what each party now brings to the table to get the right outcomes for customers. But first you need to understand what the customer wants. Do they need more oxygen in the P&L, are they reducing costs, have they spotted a business opportunity, is their IT estate too complex? “Depending on what’s driving that behaviour will ultimately depend on the right answer and whether that is to partner with a telco directly or whether that’s to use an integration partner instead,” she said.

She added that AI is changing this equation once again with customers asking “where am i going to be using that AI, where’s my data…I think [the issue is] starting to understand some of those questions to then be able to make the right decisions about who do I partner with who’s going to help me to fill perhaps the gaps in knowledge that I might have, or the gaps that I might have around my IT estate.”

Data leverage example

Soliman gave the example how telco marketing teams can benefit when vast amounts of network data and customer data are abstracted to deliver insights and develop new services. “You have the [customer] data, you have coverage heat maps, you have the status of the devices so how can I abstract this to [help] marketing promote new products and services,” he said, adding that new tools like GenAI help with this.

Marketing should be able to ask a simple question in layman terms and this massive, complex database that telcos have, with all its data points, should be able to give them actionable insights liking where to launch a service in their footprint.

Do telcos have the right culture?

Telefónica’s Kaynia said implementing cloudification and microservice architecture is not an easy task but the operator is doing this to be more efficient so it can have independently deployable components or features – the exact principle behind agile DevOps. “We cannot survive with this this,” she said. “If you’re not agile enough, it means we are not fast enough to adapt.”

And this impacts culture. “If we are not fast enough to be able to launch something deploy it independently with CI/CD and DevOps, [then] we can’t even get fast enough feedback to be able to adopt and then be able to calibrate as per our customers’ needs, which means we will be holding either ourselves back or the market back,” she said. “I see it as a fundamental enabler to have that right culture to move to the agile ways of working; to move towards DevOps, in order to achieve everything we talked about in terms of digitalisation and higher speed.”

Vodafone’s shift in core competencies

Hastings said she had seen “a real shift” at Vodafone in “bringing some of our core competencies and core capabilities back in house and being quite selective about where we do partner.” As a result, the telco is in the process of creating significant development and engineering hubs.

“When we think about things like digital transformation, but then really importantly, data transformation and look at where we have the skills where we need the talent and then marry that to culture, you start to kind of touch on quite an important dynamic between those two things,” she said, highlighting the intricate relationship between skill sets and cultural values.

Hastings underscored the significance of fostering a culture that empowers individuals to take ownership and initiative, stressing the importance of attracting and retaining talent within the organisation. “I think having the right environment to attract talent, to fill the right skills to then enable them to ultimately be successful. And ultimately help all of us to progress,” she said, emphasizing the role of a conducive environment in nurturing talent and driving collective advancement.

Acknowledging the ongoing evolution of organisational culture, she added: “Have we gotten it 100% right yet? No, I doubt any company…I hope no company would ever say that they do. Right? Because culture is always evolving, right? It’s always improving. There is always something that we can do better.”

The Hungarian operator, which has a controlling share of Vodafone in-country, says so-called 5.5G is capable of up to 10 times faster download speeds than 5G

Central European operator 4iG has successfully demonstrated the potential of the 6GHz band and 5G Advanced technology – which was only included by the ITU as licensable spectrum at WRC23 the end of last year – in the Budapest University of Technology and Economics (BME VIK) laboratory.

The telco, together with the Faculty of Electrical Engineering and Informatics of the Budapest University of Technology and Economics, is researching cutting-edge technology and said the new antenna technology based on current base stations, can offer up to ten times the download speed compared to the fastest 3.5 GHz solution currently in use.

With measurements carried out under laboratory conditions, the working group consisting of 4iG Group engineers and BME VIK researchers registered a data transmission speed of more than 10Gbps. The operator said a significant advantage of the new, so-called Extra Large Antenna Array (ELAA) antenna technology is that the 6GHz band can also be installed at existing sites and base stations to expand the network capacity “by leaps and bounds”, adapting to the 3.5 GHz coverage, new base station without installing locations.

Huawei solution

The solution ran on Huawei Technologies devices, and the operator said by using it, mid-band frequencies are capable of gigabit data transfer speeds with wider coverage. The equipment installed at the Budapest University of Technology and Economics primarily serves research purposes and, with the cooperation of 4iG’s Western Balkan subsidiaries, the test period also provides the researchers of the technical universities of Tirana and Podgorica with the opportunity to learn about and study the new technology.

Six months ago, 4iG Group chairman Gellért Jászai and Group CEO Peter Fekete signed an MoU in China with Huawei chairman Liang Hua to collaborate on 5G, despite the EU’s decision to impose security restrictions on the use of 5G equipment from “high-risk suppliers”. US Government officials subsequently met with Jászai and reportedly expressed their concerns about Huawei.

4iG Group became the majority owner of Vodafone Hungary at the beginning of last year. The telco is currently amidst the handover process of Vodafone’s technical and administrative back-end systems. In July last year, as part of a wider mobile network portfolio rejig, 4iG Group subsidiary Antenna Hungária entered into an agreement to sell MIS Omega Mobilhálózat, which owned Digi’s mobile infrastructure in the country. The new owner, state-owned Pro-M, gained 2,500 towers, active and passive radio network assets, as well as the rights and 1800MHz spectrum licences.

The path from trial to reality

“The testing of the world-first 6GHz mobile technology is in line with the 4iG Group’s innovation plans and digitalisation goals,” said 4iG Group’s mobile and 5G strategy director Pál Zarándy. “The switch to 5G technology is an entry point for 4iG, which has a strong IT background, because in addition to providing the infrastructural background, it also enables the exploitation of the most modern data transmission solutions.”

“The 4iG Group has brought the next level of mobile communication development to Hungary and Central-Eastern Europe, the 6GHz 5.5G cutting-edge technology,” he added.

“The 6GHz technology just presented is an important step in terms of the goals previously formulated in the 5G visions,” said BME VIK dean of the Faculty of Electrical Engineering and Informatics Dr Charaf Hassan. “The new frequency band accepted by the ITU helps the development of advanced, 5G-based industrial applications, the creation of smart factories and a ‘connected’ economy.”

He added: “The 6GHz radio data transmission arrangement is only an experimental demonstration. At the same time, the events of this year’s Mobile World Congress (Barcelona) and the increased industrial interest in the new technology indicate that 6GHz may soon appear in mobile networks and gigabit mobile internet will become a reality for users.”

Philippe Ensarguet’s keynote at Mobile Europe’s recent Telco to techco virtual conference was all about how telcos’ can return to growth in conversation with Annie Turner

Philip Ensarguet is a former winner of Mobile Europe’s CTO of the Year in the Trailblazer category (he then held that role at what is now Orange Business). With “a 100% software background” he is now VP of Software Engineering reporting directly to Orange’s group CTO, Laurent Leboucher. His job is both to be a strategist and an implementer, and his job recently has been “working hard on how to manage and orchestrate the new generation of telco cloud infrastructure, and telecoms shift towards cloud native and becoming a cloud-native telco”.

As a strategic thinker, he contributed to NGNM’s cloud-native manifesto and to the Cloud Native Computing Foundation’s white paper, which specifies, in great depth, telcos’ requirements to move towards being cloud nativeEnsarguet says that In his regular meetings with analysts and vendors, he finds “they are using one or the other of [those documents] as kind of backbone or map, to explain how they are working to transform themselves to meet those needs”.

He adds, “The relationship with the vendor ecosystem is super interesting because there are a lot of things to support in terms of transformation. The delivery of best practices in software, APIs and automation, for example, is far behind what we had when I was purely [working] in digital. That’s why it’s so exciting.”

The session was designed to probe why so much work has gone into telcos’ transforming themselves and continues, yet it is not reflected in new revenues or share price. So how will network’s ongoing evolution and operational transformation lead to growth? In short by a radical change in how telcos’ infrastructure, implementation and operations…

The following is an edited version of Ensarguet’s answers to the editor’s questions, for brevity and sense.

Ensarguet explains, “To be concrete on this, I want to emphasise that by definition, for instance, a 3GPP functional specification rule how [certain] network services have to work. But all the wrapping and the lifecycle around that is going to change based, for instance, on automated infrastructure, a new generation of deployment strategy, new ways of operation that are opening doors for novel, more optimised operating models.

Ensarguet said he’s not concerned that in the past so much talk was about telcos being behind Big Tech in terms of digitalisation because “it means that we can really learn and grab the best practices that enable or fast track digital and [associated] tools into the telecom ecosystem.”

He believes the big levers regarding growth are: API-isation, automation, the move from a vertical model to a horizontal one and AI – and especially generative AI. The four things are not separate, rather they impact each other. Ensarguet also thinks there are also some topics outside the ‘pure’ telco world that could have a big influence regarding opportunities for growth.

Underlay and overlay

Orange is concentrating on how best to use APIs to leverage the value from the underlay and the overlay networks to differentiate services – a huge benefit of owning the network. He notes there is a big industry focus on CAMARA, the Linux Foundation’s open-source project, including the definition of a new network API that can do two things. Firstly, retrieve information from the network and secondly configure the network.

He acknowledges that with the GSMA’s Open Gateway initiative, the emphasis has largely been on leveraging APIs for mobile connectivity, but says in the context of 5G, both fixed and mobile need to benefit from APIs. Ensarguet comments, “It’s not an option if you want to fully support the promise of what we are calling the programmable network”.

There has been some progress already on the fixed side, he says, such as “the old device policy on-demand or the CPE”. He adds that, “For standardisation, we work to establish end-to-end connectivity, for both. And it’s happening also in the open-source ecosystem. We truly believe that it will definitely help to create the API that has the most impact for the developer communities.”

So there is considerable effort in addressing the APIs in the right order. He says the industry wants to be sure that “We are prioritising the network services that would help B2B or B2B2C company to implement the cases where the API and network could bring a new superpower”.

Orange demo’d three kinds of use cases at Mobile World Congress, with Ensarguet stressing this is just one year after the launch of CAMARA:

• smooth, verified onboarding of users using their digital ID using two APIs from Orange’s production network

• location verification – using face recognition for secure payments between two people and being able to prove that the devices are at the same location. He says, “Here the network is bringing a superpower” combining its less exact location info with their GPS location

• geofencing – ID is used to provide notifications when devices enter a given area.

He says their potential is huge and highlights a Spanish company that is working on preventing gender violence. Ensarguet’s point is that it is not the APIs per se that matter, but the uses to which they are put.

Asked about the progress of network automation, he stresses, “We need to understand that the automation is mainly done with the network function technology we are using. You can automate physical network, you can automate the virtual network you can add to an automated network, but the level of the workload you are manipulating here as absolutely different…and that’s why we engage so much with this cloud-native, horizontal model transformation.”

He adds, “Extended delivery of automation and moving to the autonomous network for us is critical because it’s about saving money on operation and bringing us much more efficient operations. And here of course is where generative AI has a super-disrupting potential.

Industrial model

“We are investing a lot into what we are terming our industrial model to support the transformation from the flows and vertical silos to the horizontal one,” he says. “The idea is to push for an infrastructure, a deployment strategy and operation that’s API-driven and the others things I [am sharing].”

He explains, “We are pushing the level of the intent at a scale, where…our infrastructure is for the cloud native purpose is 100% intent-based and using the GitOps model [so] we are spinning our infrastructure in pure software.”

This approach to achieving a highly strategic foundation for infrastructure rests on the Sylva open-source project whose aim is to “an open Telco Cloud platform of reference” on which automation sits.

Ensarguet adds, “We are adding what we call the network integration factory, that is a total critical assets. The idea is that instead of relying on very specific and proprietary deployment, and lifecycle management tools, we rely on something we build that’s 100% standardised and we leverage the best practices from the digital and the IT world. Today, the network integration factory tooling zone is just a cloud native application we are deploying in our Orange central cloud…[that can]…provide the detailed framework for all the tools for deployment, lifecycle management and continuous testing.

“For us it is critical to be sure that everything has been validated before moving to production or accurate when the deployment is done. Everything about this is moving up to the operation layer and a new way operation that’s much more closer to the digital and IT.”

He continues, “A large part of this automation is thanks to the cloud-native superpower…it’s about the abilities in terms of resilience, of closed loop reconciliation, and risk management. Being able to rely on an orchestrator with such capabilities is a total game changer in the way we can automate and remediate our infrastructure.”

Growth is an ecosystem shift

A great question from the audience was, “How do you maintain the network advantage against competition from systems integrators and hyperscalers while transforming to a telco? Would you go as far as one of your competitors [T-Mobile USA] and [claim to] be an uncarrier?

Ensarguet said the first thing to stress is that integrators and hyperscalers are very important partners as well as competitors. The new, simple API business is leveraging use cases…but you can only have these benefits if you own the network. For me, that is a true differentiator.”

He concludes, “The four components [outlined above] can enable a new business model or new way of building infrastructure or consuming the services. For me [hyperscalers and integrators], are more enablers than real competitors… That’s why the industrial model we are working on right now around the infra layer, implement layer, operation layer is so important. It’s where we want to standardise and apply to mutualisation. It’s what I’m observing with our every telco peer.

“As a final thought, last Monday Orange had a cloud-native workshop where we add up to six or seven telco peers, from Europe and Asia. Basically, they told more or less the same story about the business of transversality is need of regionalisation is needed of some data. And that’s why all the same telcos are working hand-in-hand, supporting the transformation of the ecosystem because here in the new domain for a growth – new ways of implementation.

“We cannot win alone. We need the whole ecosystem. That’s why it’s so important to support the integrators, the vendors, the hardware makers, because we can only win growth for the new generation if the whole ecosystem is shifting.”

Technology, operations and management kept under one umbrella so customers don’t need to worry about platforms, operations, analytics, and reporting

Deutsche Telekom Global Carrier has introduced Magenta Security Roaming which it said offers an ecosystem of secure connectivity for all protocols currently used by its customers: 2G, 3G, 4G, 5G non-standalone (NSA) and 5G standalone (SA). For each protocol, corresponding protection layers are in place which work in unison: SS7 Firewall, Diameter Edge Agent (DEA) Firewall, Diameter End-to-End Signalling Security (DESS), phase 1, as well as Security Edge Protection Proxy (SEPP) in several configurations.

The service is available to all the wholesaler’s customers, both its own group national operator companies (NatCos), as well as operators across the globe. The new concept comprehensively addresses operators’ increasing need for low-latency, reliability and security when roaming in today’s interconnected world.

Deutsche Telekom Global Carrier provides all Magenta Security Roaming services with dedicated support and SLAs. The service is designed to help maintain business by increasing the quality of operators’ cyber-defence systems, while reducing cost and complexity, according to the operator. As roaming security will become increasingly heterogenous throughout the world, Magenta Security Roaming offers a way to connect each destination with the top security as required by both operators.

5G SA roaming

For those operators which have already enabled 5G SA roaming, Magenta Security Roaming guarantees that they have options when interconnecting with each other by choosing the security measures they need. Telcos can outsource investment and operation of 5G SA roaming with Magenta Security Roaming’s outsourced SEPP solutions.

They can also opt for hosted SEPP maintenance services, as well as “composite scenarios” that connect individual roaming partners most efficiently. These include Deutsche Telekom Global Carrier’s new Group hosted SEPP for Family & Friends services specifically dedicated to its internal (NatCos) and external operator customers.

Deutsche Telekom Global Carrier claims it is the only carrier to offer DESS, phase 1 for 4G and 5G NSA services, which guarantees end-to-end authentication of signalling messages. “The combination of Diameter Firewall and DESS, phase 1 enables the world’s most secure LTE and 5G NSA exchange between mobile operators,” stated the telco.

“Security in roaming is a major issue in our industry. For the first time, we work with 5G SA as a technology where security is built in, while we still have to protect all the other protocols effectively to ensure roaming security across the board,” said Deutsche Telekom Global Carrier VP voice and mobile solutions Nicholas Nikrouyan.

“Magenta Security Roaming is our answer to this all-or-nothing scenario with highly innovative roaming security services, as well as our world-exclusive offer of DESS, phase 1,” he said. “Our innovative roaming concept allows us to avoid 5G hubbing and move to a world where security is there by design.”

First hosted SEPP 5G SA roaming

Last October, T-Mobile US and Deutsche Telekom Global Carrier completed successful testing of 5G Standalone (5G SA) roaming, utilising the wholesaler’s Security Edge Protection Proxy (SEPP) to complete the world’s first hosted SEPP 5G SA roaming T-Mobile US and Sunrise and a direct SEPP to SEPP interconnect with AIS Thailand.

The program used Deutsche Telekom Global Carrier’s Internet Protocol Exchange (IPX) and Hosted Security Edge Protection Proxy (SEPP) solutions with Sunrise and AIS, successfully completing 5G SA roaming between the US and Switzerland and the US and Thailand.

The telco said 5G SA roaming networks will offer faster speeds, lower latency, and higher capacity compared to non-standalone (NSA) networks. SA roaming is also crucial for supporting massive IoT deployments and critical IoT applications.

The vendor sees sales and RAN market in decline in Q1 but first-quarter operating profit and earnings per share still above market expectations

Ericsson president and CEO Börje Ekholm said customers remained cautious about investing in their networks, after the vendor saw network equipment sales in Q1 2024 were down 19% from a year earlier. Meanwhile CFO Lars Sandstrom suggested Dell’Oro’s forecast that the global RAN market will decline 4% this year was “a bit optimistic as we see it now”.

Ekholm however seemed cautiously optimistic that while the global market isn’t going to take off, the company was seeing signs it will be less bad than 2023. He said if current trends continue, sales should stabilise in the year’s second half, “benefiting from recent contract wins and the normalization of customer inventory levels in North America.” He added that gross margin in the second quarter should be in the 42% to 44% range, bolstered by an improved business mix.

Despite the sales decline, markets reacted positively to Ericsson’s results due to its gross margins excluding restructuring charges improving to 42.7% in the quarter – comfortably ahead of market expectations. Net income improved to SEK 2.6 billion, from SEK 1.6 billion YoY.

Europe’s telco market needs to change

On the company’s earnings call, Ekholm pulled no punches when asked if the business is drifting without a catalyst for increased spending by operators. Firstly, he addressed the investment pause was starting to impact operator network capacity.

“The reality is we see the traffic growth in the networks continues. And you start to see – in many markets, not singling out anyone specifically, but you’re starting to see congested networks, which means that when it’s crowded, you’re in a crowded space,” said Ekholm.

“You may actually get the signal, but you can’t really use it. You have simply no capacity left in the network. We’re starting to see those signs. We start to see signs that sites are congested,” he said.

He then said what we already know – the industry has a problem with return on investments. “I think personally we need to see in-market consolidation actually start to [happen] and start to get approved. When that happens, we will get bigger scale. And it’s interesting, when you look at this from a global perspective, the average European operator is about 4.5 million subscribers,” he said.

“It’s 95 million, I believe, in the US, 300 million in India, 400 million in China,” he said. “So the scale in Europe is simply too small. So, there is consolidation needed. The second part that needs to happen, and that’s what we try to do with the Global Network Platform for network APIs, is actually to change the pricing model in the industry.”

Changing the pricing model

Ekholm said the current monthly subscription pricing model has decoupled from network traffic, network investments and so on, putting a squeeze on the operator profitability. “What we need to see happening to unlock investments is that you’re able to monetise the network features,” he said. “And that – think about it as speed, latency, could be location, could be different quality of service or differentiated experiences.”

“You can offer network slicing, for example,” he said. “We need to define that new type of use cases that unlocks those revenue streams. Otherwise, the customers, our operators, they’re not going to see growing revenues. And if they don’t see growing revenues, they’re not going to invest.”

He added: “That’s the perfect rational decision. So, I think we have that, call it, opportunity or maybe responsibility to create those new type of revenues coming out of leverage in the 5G technology in a better way. That’s why you see our investments on the Enterprise side being so important.”

In Enterprise, sales grew organically overall but declined in Global Communications Platform, impacted by a low-margin customer contract loss in Q4 and Ericsson’s decision to reduce its operations in some countries, with the impact expected to continue throughout the year. The vendor said it will continue to focus on “leveraging the current business to support the build-out of our Global Network Platform for network APIs.”

Outlook for the company

Ericsson said if current trends persist, it expects sales to stabilise during the second half of the year, benefiting from recent contract wins and the normalisation of customer inventory levels in North America.

In the second half, the vendor’s margins should benefit from its improved business mix. Ekholm said the company also remains highly focused on delivering stronger cash flow, based on its operating discipline. “While near-term dynamics are challenging, we remain fully committed to our long-term targets, and we continue to be focused on increasing shareholder value,” he said.